>> good article from Motley Fool today on LINE

http://www.fool.com/investing/general/2 ... ified.aspx

Motley Fool

By Matt DiLallo | More Articles

October 15, 2014 |

It's been a terrible month for LINN Energy LLC (NASDAQ: LINE ) investors. The company's units are off just over 25% in the past month as oil prices have fallen to their lowest level in years. This sell-off is being fueled by concerns that falling oil prices will have a big impact on LINN Energy's ability to pay its distribution at its current level, let alone grow the payout. There's just one problem with these concerns: LINN Energy is one of the best in the business at hedging its exposure to commodity prices.

Reducing risk

As the following slide from a recent investor presentation points out, 100% of LINN Energy's natural gas production is hedged through 2017.

http://g.foolcdn.com/editorial/images/1 ... _large.jpg

The concern that some have with the company is its oil hedges. While 100% of 2014's production is hedged, just 50%-60% of production is hedged over the next two years. That leaves some of the company's cash flow exposed to falling oil prices.

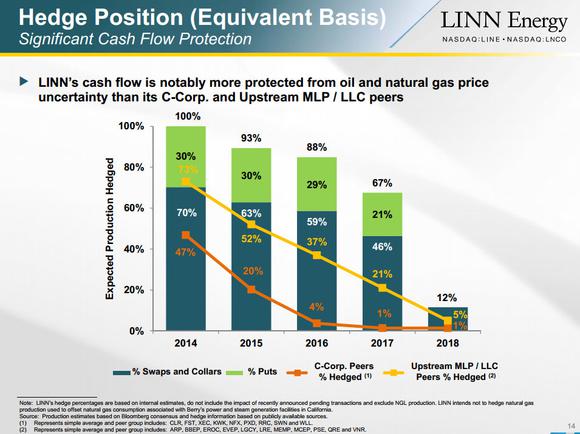

However, LINN Energy's cash flow isn't as exposed to oil as one might think. In fact, as we see in the following slide, on an equivalent basis just 7% of 2015 cash flow is at risk.

http://g.foolcdn.com/editorial/images/1 ... _large.jpg

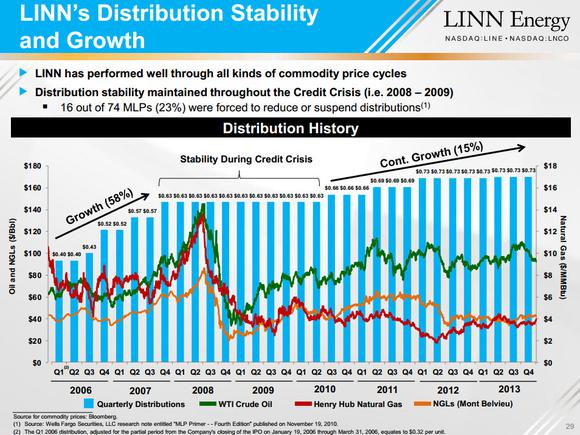

This is really important because it means that the company's distribution is on really solid ground even with oil prices tumbling. We've seen LINN Energy's strategy at work before when oil prices tumbled in 2008. The company was able to maintain a stable distribution during the economic crisis because its hedging practices shielded it from falling oil and gas prices, as we see in the following slide.

http://g.foolcdn.com/editorial/images/1 ... _large.jpg

If LINN Energy could provide its investors a stable distribution during the worst economic crisis in the last 50 years where oil prices fell about $100 per barrel then the odds are pretty good it can maintain its distribution when oil prices fall a mere 20%. In fact, the current plunge in oil prices could be a positive for LINN Energy's investors.

Taking advantage of the situation

Investors might not realize this, but last quarter LINN Energy did something that it rarely does. Its board of directors authorized management to buy back up to $250 million worth of its common units. The last time its board authorized a big buyback program was in 2008 when it authorized a $100 million unit buyback program. While the program was used sparingly the company did buy back some units at rock bottom prices. LINN Energy could use its newly authorized buyback program to take out more than 11 million units and save $32 million in future distribution payments. That would improve the company's coverage ratio by about 3%, which would further stabilize the distribution for the rest of its investors.

In addition to that LINN Energy could use the fall in oil prices to buy oil assets at a discount. Falling oil prices could force some oil companies with a lot of debt to sell assets in order to bolster their balance sheets. These assets would likely be offered at a lower sales prices than just a few months ago so LINN Energy would have the opportunity to find better deals that would really bolster its distributable cash flow. With the company's repositioning plan nearly complete it's in the perfect position to go on the offensive and start buying assets at a discount.

Investor takeaway

The recent sell-off in LINN Energy appears completely unjustified. The company's cash flow is more secure than investors realize. In fact, the current sell-off could be a very compelling opportunity for LINN Energy as it could buy back a decent chunk of its units and then go out make a really accretive acquisition that might not have been possible if oil prices didn't fall

Is LINE's 25% plunge justified?

{kind=link}

{kind=link}

{kind=link}

Re: Is LINE's 25% plunge justified?

IMO the big pullback in all four of our upstream MLPs in the High Yield Income Portfolio (BBEP, LINE, MEMP and VNR) has created a great buying opportunity for investors seeking high yield. Here is a chance to lock in very nice yields (over 10%) with some high quality companies that also have a ton of growth potential.

For those who like LINE, I recommend you take a look at LNCO. They offer regular dividends (no K-1).

For those who like LINE, I recommend you take a look at LNCO. They offer regular dividends (no K-1).

Dan Steffens

Energy Prospectus Group

Energy Prospectus Group

Re: Is LINE's 25% plunge justified?

the spread between LINE and LNCO got huge and I understand they are identical except no K-1 from LNCO so basically sold my LINE and replaced it with LNCO...........does that make sense???

Re: Is LINE's 25% plunge justified?

Yes. it makes a lot of sense. Here is the difference: With LINE you are owning "units" in a partnership and most of the cash distributions are tax deferred. You do have to recover the deferred portion as ordinary income when you sell LINE.

LNCO is a C-Corp. The "dividends" from LNCO are regular dividends, so they are currently taxable. LNCO is great for those of you that want high yield in your IRA account.

LNCO is a C-Corp. The "dividends" from LNCO are regular dividends, so they are currently taxable. LNCO is great for those of you that want high yield in your IRA account.

Dan Steffens

Energy Prospectus Group

Energy Prospectus Group